Is accumulated depreciation an intangible asset? This is a question commonly asked by individuals who are learning about accounting and financial statements. To understand whether accumulated depreciation qualifies as an intangible asset, we need to examine the nature of accumulated depreciation and the criteria for classifying assets.

Accumulated Depreciation Explained

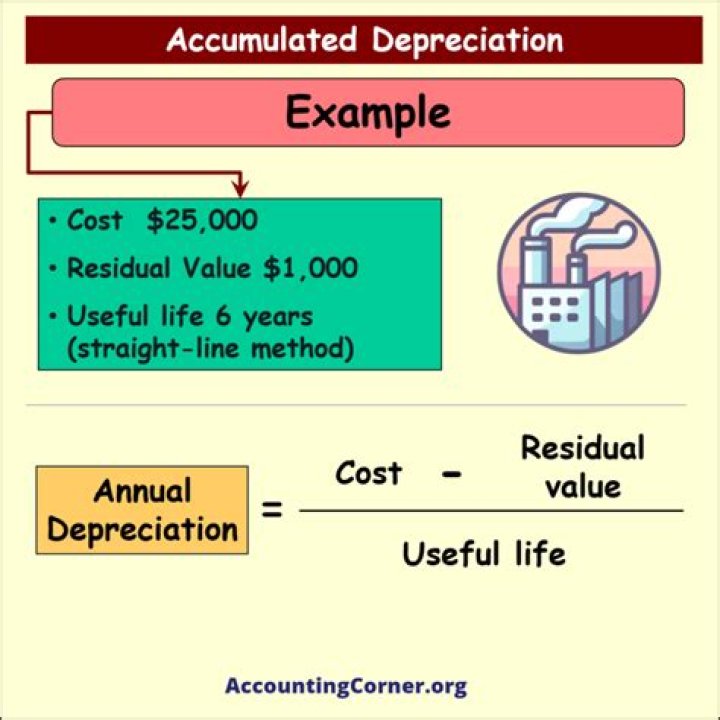

Depreciation refers to the systematic allocation of an asset’s cost over its useful life. As assets age and wear out, they lose value, and their cost is gradually expensed through depreciation. Accumulated depreciation, on the other hand, represents the total amount of depreciation expense recognized on an asset from the time it was acquired until the present.

The Nature of Intangible Assets

Intangible assets are non-physical resources that provide long-term value to a company. Examples of intangible assets include patents, trademarks, copyrights, and goodwill. These assets lack physical substance but possess legal or contractual rights that contribute to a company’s economic value.

The Classification of Accumulated Depreciation

Accumulated depreciation does not meet the criteria for being classified as an intangible asset for several reasons. Firstly, accumulated depreciation does not possess any legal or contractual rights. It does not grant exclusive control or ownership over a particular resource. Secondly, accumulated depreciation is not separable from the related tangible asset.

FAQs about Accumulated Depreciation

Table of Contents

1. Is accumulated depreciation a current asset?

No, accumulated depreciation is not a current asset. It is classified as a contra asset, reducing the book value of the related tangible asset on the balance sheet.

2. How is accumulated depreciation reported on financial statements?

Accumulated depreciation is typically listed as a deduction below the related asset’s cost on the balance sheet. It reduces the carrying value or net book value of the asset.

3. Can accumulated depreciation have a negative balance?

Yes, in certain situations when an asset’s carrying value is adjusted due to impairments or revaluations, accumulated depreciation can have a negative balance.

4. Does accumulated depreciation impact net income?

Accumulated depreciation does not directly impact net income. Instead, it affects the valuation and carrying value of the related asset, which indirectly influences depreciation expense and, subsequently, net income.

5. What happens when an asset is fully depreciated?

When an asset is fully depreciated, its accumulated depreciation equals its original cost, resulting in a zero net book value. It no longer carries any value on the company’s financial statements.

6. Is accumulated depreciation considered a liability?

No, accumulated depreciation is not considered a liability. Liabilities represent obligations or debts owed by a company, while accumulated depreciation is simply a reduction in the value of an asset.

7. Can accumulated depreciation be recovered?

Accumulated depreciation cannot be directly recovered since it is not a separate asset. However, if an asset is sold or disposed of, any cash proceeds received may partially recover the asset’s original cost.

8. Does accumulated depreciation impact cash flows?

Accumulated depreciation does not directly affect cash flows. However, depreciation expense, which contributes to accumulated depreciation, is considered a non-cash expense in the statement of cash flows.

9. Can accumulated depreciation be transferred to another asset?

Accumulated depreciation is specific to the asset it is associated with and cannot be transferred to another asset. Each asset has its own separate accumulated depreciation account.

10. Is accumulated depreciation a permanent account?

Yes, accumulated depreciation is a permanent account, meaning its balance carries forward from one accounting period to the next until the related asset is disposed of or fully depreciated.

11. Why is accumulated depreciation important?

Accumulated depreciation is important as it allows companies to accurately report the carrying value of their assets, reflecting their true economic value over time, and enabling more informed financial analysis and decision-making.

12. Does accumulated depreciation affect taxes?

Accumulated depreciation indirectly affects taxes. Tax authorities often require companies to adjust their taxable income by considering depreciation expense, which contributes to accumulated depreciation, when calculating tax liabilities.

In conclusion, accumulated depreciation is not classified as an intangible asset. It differs in nature from intangible assets, lacking legal or contractual rights and separability from the related tangible asset. Instead, accumulated depreciation is considered a contra asset, reducing the carrying value of the asset on the balance sheet. Understanding the distinction between accumulated depreciation and intangible assets is crucial for accurate financial reporting and analysis.